Global Finance

Cross-Border Payments Explained: From Correspondent Banking to Stablecoin Rails

Reah Team

When a business needs to pay a supplier in another country, the transaction looks simple on the surface: money leaves one account and arrives in another. What happens in between is considerably more complicated and expensive than most finance teams realize.

How a traditional cross-border payment works

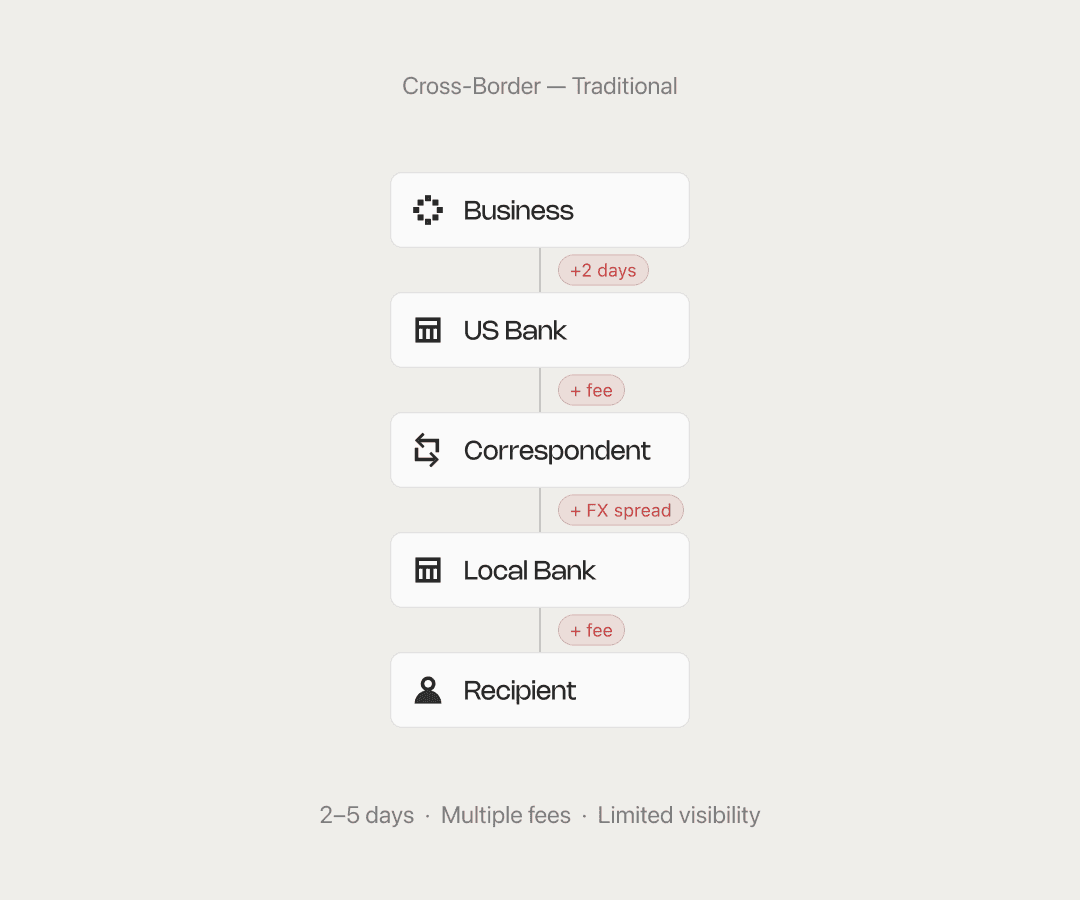

Most international payments don't travel directly from sender to recipient. Instead, they move through a chain of correspondent banks — intermediary financial institutions that hold accounts with each other and pass transactions along.

Here's what a typical payment from a US business to a supplier in Southeast Asia might look like:

The sending business instructs its US bank to transfer funds.

The US bank routes the payment to a correspondent bank with a relationship in the destination region.

That correspondent bank may pass it to another intermediary closer to the destination country.

The final bank in the chain credits the recipient's account.

Each step introduces processing time, fees, and potentially a foreign exchange conversion. By the time the payment arrives, the recipient receive less than expected — and the sender limited visibility into where the funds are or when they will settle.

Why it's slow and expensive

Settlement windows. Traditional interbank settlement systems operate on business-day schedules. Payments initiated on a Friday afternoon may not settle until Monday or Tuesday. Cut-off times vary by bank and region, and a payment that misses a cut-off can sit for an extra day.

FX markups hidden in the spread. When a payment crosses currencies, banks apply a foreign exchange conversion. The rate applied is rarely the mid-market rate. Instead, banks build in a spread that functions as an additional fee — one that often isn't disclosed as a separate line item.

Intermediary fees. Each correspondent bank in the chain may deduct a processing fee before passing the payment onward. The sender often has limited visibility into how many intermediaries will be involved or what each will charge.

The result is a payment process that is slow, expensive, and difficult to track end-to-end.

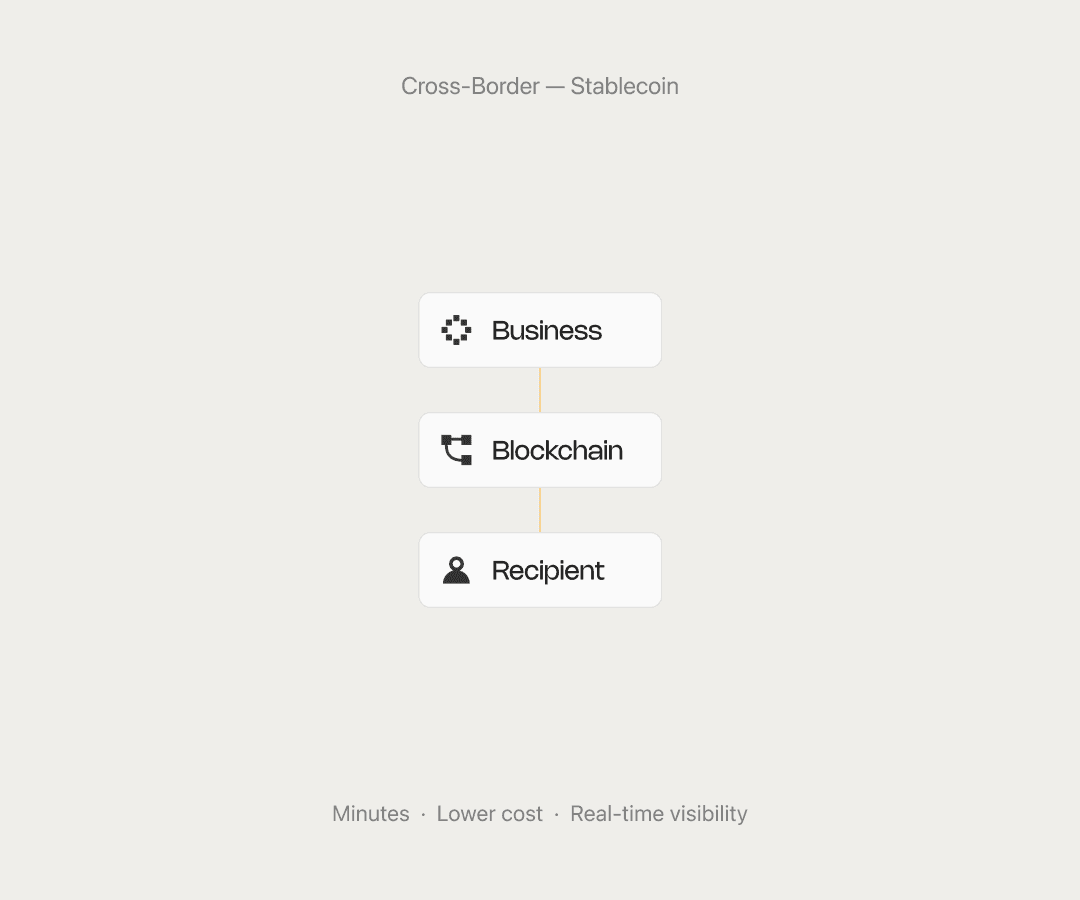

What stablecoin rails change

When used as a payment rail, stablecoins can significantly reduce reliance on correspondent banking networks. A transaction can settle in minutes rather than days, while both sender and recipient gain real-time visibility into its status through a public ledger.

Fewer intermediaries also mean fewer opportunities for delays and fee deductions. When foreign exchange conversion is required, it can often be executed at the point of transaction with greater transparency than traditional banking rails.

For businesses making recurring cross-border payments, including supplier payments, contractor payroll, and inter-company transfers, the practical impact can be substantial: faster settlement, lower costs, and improved visibility.

What this means for finance teams

The practical barrier to adopting stablecoin rails for cross-border payments has historically been operational, not conceptual.

Finance teams understand the potential. What they need is infrastructure that makes it manageable: execution that routes automatically, controls that enforce policy, and audit records that satisfy accounting and compliance requirements.

Correspondent banking will remain a critical part of the global financial system for years to come.

But businesses no longer have to choose between global reach and operational efficiency. For companies already moving significant volume across borders, the infrastructure to move money faster, at lower cost, and with greater visibility already exists.

Reah is a financial operating system for global businesses — fiat banking, stablecoin treasury, cross-border payments, and AI-native execution on one ledger. Lean more at Reah.com

Share this article